Whether you manage the care of an elderly family member or obtain professional in-home care, there are some tax benefits for doing so. The IRS has different options for your consideration and, of course, there are certain requirements that must be met.

If you are paying for more than half of an elderly dependent’s living expenses and the dependent has a gross income under $4,300 (excluding Social Security) you can claim him or her as a dependent for tax purposes. “Living expenses” are defined as food, housing, utilities, health care, repairs, clothing and travel. The tax credit can be as much as $500.

If family members split the expenses, only one can claim the dependent – but it must be one who has contributed at least 10 percent of the support costs. This is called a “multiple support agreement” among family members who are in this situation.

There are additional potential tax benefits for medical deductions. If an adult child claims a parent as a dependent and pays expenses not reimbursed by insurance and the expenses (plus the family’s other medical expenses) exceed 7.5 percent of the adult child’s Adjusted Gross Income (AGI) the excess is deductable.

In-home care might also be covered under the Dependent Care Tax Credit. These credits can be worth as much as $4,000. To qualify, the dependent must be physically or mentally incapable of self-care and must have lived in your household for more than six months.

It is also possible that you can use funds from a Health Savings Account (HSA) or Flexible Savings Account (FSA) if your employer provides one. You can use these funds if the dependent is an IRS-qualified dependent. NOTE: If you use funds from an HSA or FSA, you cannot take a tax deduction for these expenses.

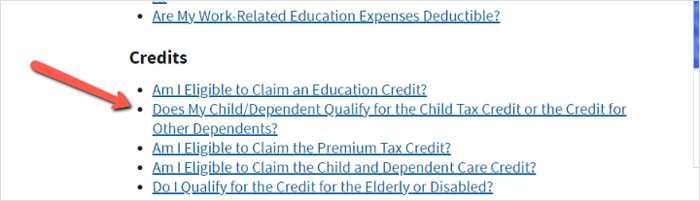

The IRS has an interactive tool that will help you determine if your loved-one qualifies as a dependent. Go to www.IRS.gov/help/ita, scroll down to “Credits,” and click on “Does My Child/Dependent Qualify for the Child Tax Credit or the Credit for Other Dependents?”